Adecco reports solid Q3 2012 results Dienstag, 06. November 2012 - 07:02

Adecco reports solid Q3 2012 results

The Group achieves strong profitability on the back of price discipline and cost control

Third quarter 2012 HIGHLIGHTS

- Revenues of EUR 5.3 billion, flat year-on-year (-5% organically1)

- Gross margin at 17.9%, up 70 bps year-on-year (+50 bps organically)

- SG&A down 2% year-on-year, organically and excluding restructuring costs

- EBITA2 excluding restructuring costs at EUR 232 million

- EBITA margin at 4.4%, up 10 bps compared to last year, excluding restructuring costs

- Restructuring costs amounted to EUR 22 million of which EUR 19 million related to France

- Net income of EUR 118 million, down 18%

- Operating cash flow of EUR 284 million in the first nine months of 2012 (EUR 217 million in 2011)

Key figures Q3 2012

| in EUR millions |

reported |

reported growth |

constant currency growth |

| Revenues |

5,279 |

0% |

-5% |

| Gross profit |

947 |

+4% |

-1% |

| EBITA excluding restructuring costs |

232 |

+2% |

-3% |

| EBITA |

210 |

-7% |

-12% |

| Operating income |

197 |

-8% |

-12% |

| Net income |

118 |

-18% |

Zurich, Switzerland, November 6, 2012: Adecco Group, the world’s leading provider of Human Resources solutions, today announced results for the third quarter of 2012. Revenues were flat or down 5% organically, to EUR 5.3 billion. The gross margin was 17.9%, an increase of 70 bps versus the prior year and up 50 bps organically. Continued strong cost control resulted in 2% lower SG&A, on an organic basis and excluding restructuring costs. The Q3 2012 EBITA margin excluding restructuring costs was 4.4%, up 10 bps compared to the EBITA margin of Q3 last year. Net income was down 18% to EUR 118 million. The Group generated operating cash flow of EUR 284 million in the first nine months of 2012.

Patrick De Maeseneire, CEO of the Adecco Group said: “Our focus on price discipline continues to show in our results. I am pleased to report an increase of 50 bps organically of our gross margin to 17.9%. At the same time, we remained disciplined on the cost-side. SG&A was down 2% year-on-year organically and excluding restructuring costs. As a consequence the EBITA margin was up 10 bps to 4.4%, when excluding the restructuring costs. Looking at developments from a geographical viewpoint, we continue to witness diverse trends across our markets. In France, we maintained good profitability despite declining revenues. In North America revenue growth accelerated to 3% organically also driven by good growth in the IT segment. The UK held up well and we outperformed the market in Germany. Organic growth in Japan further weakened, as last year’s results included a few large projects. Elsewhere, we performed well in the Benelux against the market and the same holds true for the Nordics. In Italy and Iberia, the revenue decline rate stabilised. Growth of LHH, our career transition and talent development business accelerated to 9% organically in Q3 2012, with strong profitability. While the outlook remains uncertain, we are convinced we have the global reach, a strong combination of businesses and a disciplined approach to pricing and cost control which will get us to our EBITA margin target of above 5.5% midterm.”

Q3 2012 FINANCIAL PERFORMANCE

Revenues

Group revenues in Q3 2012 were EUR 5.3 billion, flat or down 5% in constant currency. Organically, revenues were down 5%. Permanent placement revenues amounted to EUR 85 million, a decrease of 10% organically, while revenues from the counter-cyclical career transition (outplacement) business totalled EUR 65 million, up 5% organically.

Gross Profit

In Q3 2012, gross profit amounted to EUR 947 million and the gross margin was 17.9%, up 70 bps compared to the prior year’s third quarter. Organically the gross margin was up 50 bps in the quarter under review. Temporary staffing had an organic 30 bps positive impact on the gross margin. Organically, permanent placement had a neutral impact on the gross margin, whereas the impact was +10 bps from outplacement and +10 bps from other activities.

Selling, General and Administrative Expenses (SG&A)

SG&A in Q3 2012 amounted to EUR 737 million, an increase of 8% or 2% in constant currency compared to Q3 2011. SG&A was 2% lower year-on-year on an organic basis and excluding restructuring costs. Restructuring costs for France and Germany were EUR 20 million in the quarter under review. In addition, restructuring costs incurred for the consolidation of several data centres in North America amounted to EUR 2 million in Q3 2012. Sequentially, SG&A was down 2% on an organic basis and when excluding restructuring costs. Organically, FTE employees decreased by 3% (-1,000) compared to the third quarter of 2011. The branch network, on an organic basis, decreased by 2% (-100 branches) compared with the third quarter of 2011. At the end of the third quarter of 2012, the Adecco Group had close to 33,000 FTE employees and operated a network of over 5,500 branches.

EBITA

In the period under review, EBITA was EUR 210 million compared with EUR 226 million reported in the third quarter of 2011. The Q3 2012 EBITA margin was 4.0% compared to 4.3% in Q3 2011. EBITA excluding restructuring costs was EUR 232 million in Q3 2012 and the margin was 4.4%, up 10 bps compared to the EBITA margin of Q3 2011.

Amortisation of Intangible Assets

Amortisation in Q3 2012 was EUR 13 million, unchanged from Q3 2011.

Operating Income

In Q3 2012, operating income was EUR 197 million. This compares to EUR 213 million in the third quarter of 2011.

Interest Expense and Other Income / (Expenses), net

The interest expense amounted to EUR 19 million in the period under review, the same as in Q3 2011. Other income / (expenses), net was an expense of EUR 1 million in Q3 2012, compared to income of EUR 2 million in the third quarter of 2011. Interest expense is expected to be around EUR 80 million for the full year 2012.

Provision for Income Taxes

The effective tax rate in the period under review was 33% compared to 26% in Q3 2011.

Net Income / Net Income attributable to Adecco shareholders and EPS

In the period under review, net income / net income attributable to Adecco shareholders was EUR 118 million. This compares to EUR 145 million in Q3 2011. Basic EPS in Q3 2012 was EUR 0.62 (Q3 2011: EUR 0.76).

Cash flow, Net Debt3 and DSO

Cash generated from operating activities amounted to EUR 284 million in the first nine months of 2012 and compares to EUR 217 million in the same period last year. The Group paid dividends of EUR 256 million and capital expenditure amounted to EUR 71 million in the first nine months of 2012. Net debt at the end of September 2012 was EUR 1,101 million compared to EUR 892 million at year end 2011. DSO was 55 days in the third quarter of 2012, compared to 56 days in the same period last year.

Currency Impact

In Q3 2012, currency fluctuations had a positive impact on revenues of approximately 5%.

SEGMENT PERFORMANCE

Revenues in France amounted to EUR 1.3 billion, down 16% compared to Q3 2011. Permanent placement revenues were down 15%. In the quarter under review, EBITA was EUR 35 million compared to EUR 64 million in Q3 2011. The EBITA margin was 2.6% in Q3 2012, down 140 bps compared to the prior year’s third quarter. Excluding EUR 19 million restructuring costs incurred in Q3 2012, the EBITA margin was at a solid 4.1%, compared to 4.0% a year ago. The plans to combine the business of the Adecco and Adia brands under the single brand of Adecco are fully on track.

In North America, Adecco’s revenues increased 3% organically to EUR 977 million in Q3 2012. General Staffing revenues increased 2% in constant currency and Professional Staffing revenues grew by 5% organically. The North American IT Professional Staffing segment grew 6% year-on-year organically in Q3 2012, driven by solid growth in the US of 8% organically. Revenues developed solidly in Finance & Legal and Medical & Science, up 6% and 20% respectively year-on-year, both in constant currency. The Engineering & Technical segment was flat in constant currency. Permanent placement revenues continued to develop strongly, up 15% organically. EBITA was EUR 41 million and the EBITA margin was 4.3%, up 20 bps compared to Q3 2011. Excluding EUR 2 million restructuring costs incurred for the consolidation of several data centres in North America, the EBITA margin was at 4.4% in Q3 2012.

In the UK & Ireland, revenues were up 9% in constant currency to EUR 517 million. Permanent placement revenues were down 31% in constant currency, compared with a strong third quarter in 2011. EBITA was EUR 4 million in Q3 2012, and the EBITA margin was 0.7% compared to an EBITA margin of 2.9% in Q3 2011. In the quarter under review profitability was impacted by the sponsorship costs for the London Summer Olympics.

In Germany & Austria, Q3 2012 revenue development continued to be ahead of the market. Revenues declined by 1% organically to EUR 418 million, compared against a strong base last year (Q3 2011: +23% year-on-year revenue growth). EBITA amounted to EUR 35 million and the EBITA margin was 8.3% compared to 9.6% in Q3 2011. Restructuring costs to optimise the cost base amounted to EUR 1 million in the quarter under review. Excluding these costs, the Q3 2012 EBITA margin was 8.5%.

In Japan, revenues were down 5% in constant currency to EUR 379 million. Organically revenues were down 15% and were impacted by the completion of several outsourcing projects. Profitability remained strong. EBITA was EUR 23 million and the EBITA margin was 6.1%, up 60 bps compared to the third quarter of 2011. The acquired company VSN Inc. continued to develop well. VSN added 20 bps to the EBITA margin in Japan in Q3 2012.

Revenues in Italy declined by 14% in Q3 2012, compared against a high base of Q3 last year when revenues increased +19% year-on-year. Italy achieved a strong EBITA margin of 5.7% in Q3 2012, down only 60 bps year-on-year, despite the decline in revenues.

In Q3 2012, revenues in Benelux decreased by 3%. Revenue development was in line with the market in the Netherlands, but ahead of the market in Belgium. The region achieved solid profitability with an EBITA margin of 5.1% in Q3 2012, driven by both the Netherlands and Belgium.

Revenues in the Nordics were up 6% in constant currency. Revenues in Sweden were down single-digit year-on-year in Q3 2012, but solidly increased in Norway, Denmark and Finland. The EBITA margin in Q3 2012 was 4.6%.

In Iberia revenues declined by 12% as economic conditions in the region remained challenging. Revenues in Australia & New Zealand as well as in Switzerland declined 11% in constant currency in Q3 2012.

The Emerging Markets grew 9% in constant currency to EUR 466 million, mainly driven by Latin America. The EBITA margin was 3.5%, up 80 bps when compared to the same period last year.

Revenues of Lee Hecht Harrison (LHH), Adecco’s career transition and talent development business were EUR 76 million, up 34% in constant currency and up 9% organically compared to Q3 2011. EBITA was EUR 19 million and profitability remained strong, as the EBITA margin reached 24.3%. The integration of DBM, which the Group acquired and included in the results since September last year, has been successfully completed and no further integration costs have been incurred during Q3 2012.

BUSINESS LINE PERFORMANCE

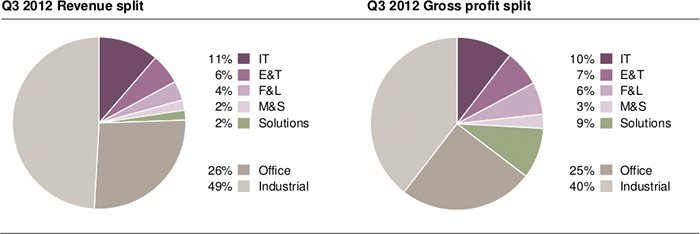

Adecco’s revenues in the General Staffing business (Office & Industrial) decreased by 7% organically to EUR 4.0 billion. Revenues in the Industrial business were down 9% in constant currency (-10% organically). In France, revenues declined by 16% organically in Q3 2012 and in Italy by 15%. Germany & Austria was down 2% organically year-on-year. In constant currency, revenues in Industrial in North America grew 1% in Q3 2012. In the Office business, revenues were down 2% in constant currency. Whereas revenues in Japan were down 17%, revenues in North America continued to hold up well and were up 4% and in the UK & Ireland revenues increased double-digit, all in constant currency.

Professional Staffing 4 revenues increased 2% in constant currency (1% organically). Revenues in North America were up 5% organically, same as in the UK & Ireland, where revenues were up 5% in constant currency. Revenues in France were down 9%.

In Information Technology (IT), revenues were flat in constant currency (+2% organically). In North America, revenues grew by 6% organically, with the US IT Professional Staffing segment growing by 8% organically. Revenues in the UK & Ireland grew by 6% in constant currency.

Adecco’s Engineering & Technical (E&T) business was up 9% in constant currency (3% organically). In Germany & Austria revenues grew by 5%, while in France revenues grew by 6%. In North America revenues were flat compared to the same period last year, whereas the UK & Ireland grew strongly double-digit, both in constant currency.

In Finance & Legal (F&L), revenues were down 2% in constant currency. Revenues in North America increased 6%, while business in the UK & Ireland remained difficult, with revenues declining by 15% in Q3 2012, all in constant currency.

In Q3 2012, revenues in Medical & Science (M&S) were down 1% in constant currency (-3% organically). While revenues in North America were up 20%, revenues in the Nordics declined by 16%, both in constant currency. Revenues in France were down 15% in the quarter under review.

In the third quarter of 2012, revenues in Solutions 5 were up 26% in constant currency or up 8% organically. Revenue growth in MSP (Managed Service Programmes) and VMS (Vendor Management System) continued to be double-digit in constant currency.

MANAGEMENT OUTLOOK

Developments continue to be diverse across the different geographies. In September, revenues declined by 3% organically and adjusted for business days. Revenue growth at the beginning of the fourth quarter slightly weakened from the -5% organically seen in Q3 2012, driven by the UK, Germany, and the Emerging Markets. The revenue decline rate in France and Japan stabilised. In North America revenue growth continued to develop well driven by both General and Professional Staffing.

Given current trends, we continue to focus on price discipline and the tight alignment of the cost base to revenue developments. Consequently, in Q4 2012, we anticipate further EUR 15 million investments to optimise the cost base, in addition to the already announced EUR 65 million for 2012 (EUR 45 million for France, EUR 10 million for other countries, EUR 10 million for the data centre consolidation in North and South America), of which EUR 37 million have been incurred in the first 9 months of this year. SG&A in Q4 2012 is expected to remain approximately in line with the third quarter of 2012, on an organic basis and when excluding restructuring costs.

With the disciplined approach to pricing and cost control and building further on Adecco’s strategic priorities, we remain convinced that we are on track to reach an EBITA margin of above 5.5% midterm.

Management changes

Mark Du Ree, the current Regional Head of Japan is retiring at the end of 2012. The Board of Directors and the Executive Committee would like to thank Mark for his achievements and for his commitment to the Adecco Group over the past 27 years. Mark has been the Country Manager of Adecco Japan since 2002 and he led the successful build-up and strong profitability of Adecco in Japan during this time.

Effective as of January 1, 2013, Christophe Duchatellier will take on an extended role as the Regional Head of Asia and Japan and will join the Adecco Group Executive Committee. Christophe joined the Adecco Group in 2010, after 18 years with Michael Page, where in his latest role he was the Regional Managing Director of Europe and member of the Executive Board. Upon joining Adecco, Christophe initially managed the Professional Staffing business in France and at the beginning of 2012 was appointed Regional Head of Asia.

Update on the share buyback programme

In June 2012, the Company launched a share buyback programme of up to EUR 400 million on a second trading line with the aim of subsequently cancelling the shares and reducing the share capital. The share buyback commenced in mid-July 2012. To date, the Company has acquired 2 million shares for a total consideration of EUR 76 million under this programme.

For further information please contact:

Adecco Corporate Investor Relations

Investor.relations@adecco.com or +41 (0) 44 878 89 89

Adecco Corporate Press Office

Press.office@adecco.com or +41 (0) 44 878 87 87

Q3 2012 Results Conference Calls

There will be a media conference call at 9 am CEST as well as an analyst conference call at 11 am CEST, details of which can be found in the Investor Relations section on our website.

| UK / Global | + 44 (0)203 059 58 62 |

| United States | + 1 866 291 41 66 |

| Cont. Europe | + 41 (0)91 610 56 00 |

Financial Agenda 2012/2013

|

March 13, 2013 |

|

April 18, 2013 |

|

May 7, 2013 |

|

August 8, 2013 |

|

November 6, 2013 |

Forward-looking statements

Information in this release may involve guidance, expectations, beliefs, plans, intentions or strategies regarding the future. These forward-looking statements involve risks and uncertainties. All forward-looking statements included in this release are based on information available to Adecco S.A. as of the date of this release, and we assume no duty to update any such forward-looking statements. The forward-looking statements in this release are not guarantees of future performance and actual results could differ materially from our current expectations. Numerous factors could cause or contribute to such differences. Factors that could affect the Company’s forward-looking statements include, among other things: global GDP trends and the demand for temporary work; changes in regulation of temporary work; intense competition in the markets in which the Company operates; integration of acquired companies; changes in the Company’s ability to attract and retain qualified internal and external personnel or clients; the potential impact of disruptions related to IT; any adverse developments in existing commercial relationships, disputes or legal and tax proceedings.

About the Adecco Group

The Adecco Group, based in Zurich, Switzerland, is the world’s leading provider of HR solutions. With close to 33,000 FTE employees and over 5,500 branches, in over 60 countries and territories around the world, Adecco Group offers a wide variety of services, connecting close to 700,000 associates with over 100,000 clients every day. The services offered fall into the broad categories of temporary staffing, permanent placement, career transition and talent development, as well as outsourcing and consulting. The Adecco Group is a Fortune Global 500 company.

Adecco S.A. is registered in Switzerland (ISIN: CH0012138605) and listed on the SIX Swiss Exchange (ADEN).

| 1 | Organic growth is a non US GAAP measure and excludes the impact of currency, acquisitions and divestitures. |

| 2 | EBITA is a non US GAAP measure and refers to operating income before amortisation of intangible assets. |

| 3 | Net debt is a non US GAAP measure and comprises short-term and long-term debt less cash and cash equivalents and short-term investments. |

| 4 | Professional Staffing refers to Adecco’s Information Technology, Engineering & Technical, Finance & Legal, and Medical & Science businesses. |

| 5 | Solutions include revenues from Human Capital Solutions, Managed Service Programmes (MSP), Recruitment Process Outsourcing (RPO) and Vendor Management System (VMS). |