Barry Callebaut Group 9-Month Key Sales Figures, Fiscal Year 2025/26 Donnerstag, 09. Juli 2026 - 06:58

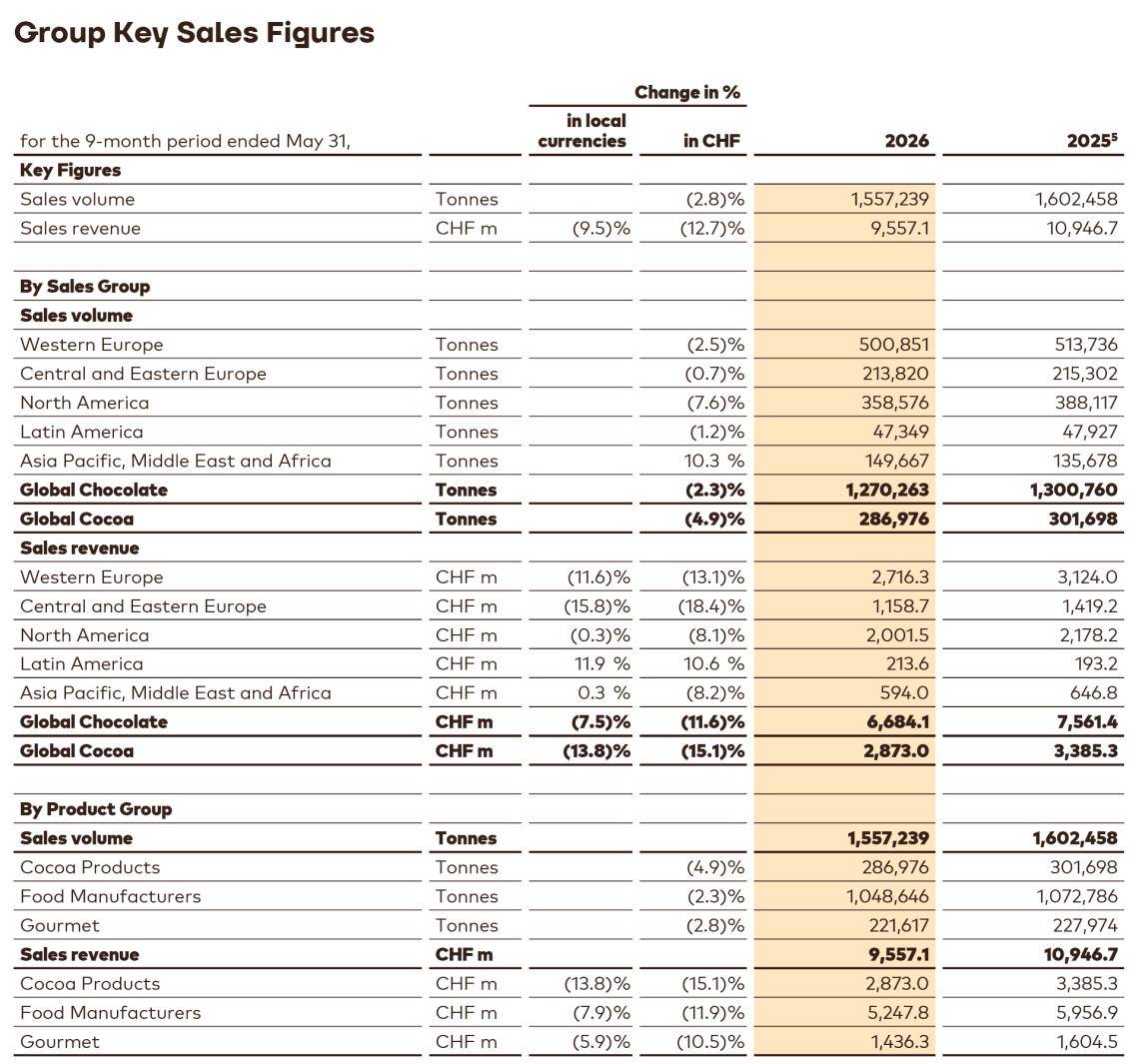

Group volume declined by -2.8% for the first nine months, turning positive in Q3 (+5.7%) for the first time in over two years

Global Chocolate volumes decreased by -2.3% for the nine months, turning positive in Q3 (+3.2%) due to continued momentum in AMEA and restoring service levels in North America

The global chocolate market remains challenging, declining by -4.4%1 in Q3, with improvement expected to be gradual

Global Cocoa volumes declined by -4.9% for the nine months, with growth accelerating to +18.0% in Q3 as the strong market correction in cocoa prices earlier in the year elevated demand

Sales revenue decreased by -9.5% in local currencies in the first nine months (-12.7% in CHF) to CHF 9.6 billion, reflecting lower year-on-year cocoa bean-related pricing

Focus for Growth action plan launched in June to strengthen Barry Callebaut’s fundamentals and leadership position as a value-added, end-to-end chocolate and cocoa solutions provider

EUR 849 million bond buyback completed in June, supporting the Group's ongoing journey to deleverage and reduce financing costs

FY 2025/26 outlook: Expect a volume decrease of around -1%. Maintain guidance for a mid-teens decrease in EBIT recurring2 and <3x Net Debt/EBITDA recurring3

1Source: Nielsen volume growth excluding e-commerce – 26 countries, February - April/May 2026. Data subject to adjustment to match Barry Callebaut's reporting period. Nielsen data only partially reflects the out-of-home and impulse consumption.

2On a recurring basis in local currencies.

3Working cocoa bean price assumption of around GBP 3,000.

Barry Callebaut Group sales volume decreased by -2.8% to 1,557,239 tonnes for the first nine months of the fiscal year 2025/26 (ended on May 31, 2026). Sales volume growth turned positive in the third quarter (+5.7%), reflecting elevated demand in Global Cocoa following the market correction earlier in the year, continued momentum in AMEA and progress in restoring service levels in North America.

Global Chocolate saw a -2.3% volume decrease in an overall declining chocolate confectionery market according to Nielsen (-5.6% in first nine months, -4.4% in Q3)4. Volume development for Food Manufacturers (-2.3%) was impacted by challenging market demand dynamics and supply disruption in North America in the first half, with a return to growth in the third quarter. Volumes in Gourmet also decreased for the nine months (-2.8%) as the declining cocoa bean price environment resulted in intense competitive dynamics.

Looking at regional performance within Global Chocolate, Asia Pacific, Middle East and Africa (AMEA, +10.3%) was the strongest contributor to volume performance. Market share gains in China, continued momentum in India and customer wins in Australia were partly offset by market pressure in Japan and South Korea. Volumes declined slightly in Central and Eastern Europe (-0.7%) as growth for regional and local Food Manufacturers was offset by a challenging environment for large Global Accounts. Latin America saw slightly negative volume growth (-1.2%), mainly due to phasing effects in the third quarter. Volume development in Western Europe (-2.5%) remained impacted by challenging market dynamics, with a return to slightly positive growth in the third quarter. North America reported a volume decrease of -7.6% as a result of network supply disruption and challenging market dynamics, with volumes turning positive in the third quarter as the business continues to rebuild service levels and respond to growing customer contracts and orders.

Global Cocoa saw a -4.9% decrease in sales volume, with growth turning strongly positive in the third quarter (+18.0%). The recent acceleration reflects elevated demand following the cocoa market correction earlier in the year, combined with a low base of comparison. Cocoa powder saw strong momentum, particularly in Latin America and Asia, with some customer restocking, while Global Cocoa also benefited from one-off cocoa butter opportunities in the third quarter.

Sales revenue amounted to CHF 9,557.1 million, a decrease of -9.5% in local currencies (-12.7% in CHF) reflecting lower volume and negative cocoa bean-linked pricing. In the third quarter, sales revenue decreased by -21.0% in local currencies (-23.4% in CHF), with pricing declining significantly as a result of lower cocoa bean prices.

4 Source: Nielsen volume growth excluding e-commerce – 26 countries, September 2025 - April/May 2026. Data subject to adjustment to match Barry Callebaut's reporting period. Nielsen data only partially reflects the out-of-home and impulse consumption.

In June, Barry Callebaut launched Focus for Growth, an action plan to strengthen Barry Callebaut’s fundamentals and leadership position as a value-added, end-to-end chocolate and cocoa solutions provider. During the third quarter, the Group took targeted steps to further enhance regional empowerment while maintaining the strong global functional alignment established over recent years. This includes evolving selected functional capabilities and teams to be closer to regional business execution, enabling greater speed and agility in commercial and go-to-market activities. As part of these changes, effective September 1, 2026, the MENA (Middle East & North Africa) & SEWA (South East & West Africa) country clusters will transition from AMEA to CEE, reflecting geographic proximity, customer preferences and supply chain interdependencies. As a result, from fiscal year 2026/27, CEE will become CEMEA (Central & Eastern Europe, Middle East & Africa), while AMEA will become Asia Pacific (APAC).

In June, Barry Callebaut completed a bond buyback tender on the Group’s outstanding Senior Guaranteed Euro-denominated Notes issued by Barry Callebaut Services NV, with a final acceptance amount of EUR 849 million. The bond buyback enables the group to further reduce its gross debt, strengthen its credit metrics and supports the ongoing journey to deleverage and reduce financing costs. As a result of the transaction, the Group will incur an upfront cost of around CHF 15 million in fiscal year 2025/26. Bondholders can find more information in the Final Results Announcement, which is available on the Group’s Debt Investor webpage.

For fiscal year 2025/26, the Group now expects a volume decrease of around -1%, at the upper end of its previously guided range. Barry Callebaut maintains its profitability guidance, with an expected mid-teens decrease in EBIT recurring in local currencies. Given the around CHF 15 million expected upfront cost from the recent bond buyback, the Group expects to recover around half of the absolute EBIT decrease at the Profit before tax level in local currencies. Deleverage progress is expected to continue with a plan to reach <3.0x Net debt / EBITDA recurring, with a working cocoa bean price assumption of around GBP 3,000.

| Date: | Thursday, July 9, 2026, from 09:00am CEST |

This will be a virtual presentation for analysts and investors, hosted by Hein Schumacher, CEO and and Peter Vanneste, CFO, which can also be followed via telephone or webcast. Dial-in and access details can be found here.

Financial Calendar for Fiscal Year 2025/26(September 1, 2025 to August 31, 2026)

| Full-Year Results 2025/26 | November 4, 2026 |

| Annual General Meeting 2025/26 | December 9, 2026 |

- Press Release

- Presentation

5Certain customers have been shifted to a different product group to better serve them. The minor reallocation represented less than 1% of the total volume and sales revenue in fiscal year 2024/25.

During the first nine months of fiscal year 2025/26, terminal market6 prices for cocoa beans declined as a sizable second consecutive cocoa surplus continued to materialize. On average, cocoa bean prices decreased by -47% versus the prior-year period and closed the period at GBP 2,954. The period saw strong main crop arrivals in West Africa, alongside a good start to the mid-crop and sustained pressure on cocoa grinding in Q4 and Q1 of the calendar year, aiding further replenishment of global stocks.

Global sugar prices averaged -19% lower year-on-year, as improving supply across major producing regions outpaced steady demand, leading to an anticipated global sugar surplus in the 2025/26 crop cycle. In Europe, sugar prices declined -14% despite reduced plantings, reflecting higher than expected yields for the 2025/26 campaign and weaker world market prices, which slowed exports and encouraged imports.

Dairy prices declined by -6% compared to the previous year. Abundant milk supply growth globally, particularly in Europe, has weighed on stocks and prices. More recently, strong protein demand has supported skimmed milk powder and whey markets, while butter remains in surplus.

6Source: London terminal market prices for 2nd position, September 2025 to May 2026. Terminal market prices exclude Living Income

Differential (LID) and country differentials.

About Barry Callebaut Group:

With annual sales of about CHF 14.8 billion in fiscal year 2024/25, the Zurich-based Barry Callebaut Group is the world’s leading solutions provider of high-quality chocolate experiences across the full spectrum of chocolate, cocoa, cacao coatings and non-cocoa alternatives – from sourcing and processing cocoa beans to crafting premium chocolates, fillings and decorations. The Group operates more than 60 production facilities worldwide and employs a diverse, committed workforce of over 13,000 people. Barry Callebaut serves as a trusted partner for the entire food industry, from large-scale food manufacturers to artisanal and professional users such as chocolatiers, pastry chefs, bakers, hotels, restaurants and caterers with Callebaut® as its main global brand. The Barry Callebaut Group is dedicated to making sustainable chocolate the norm – helping secure the future of cocoa and improving the livelihoods of cocoa farmers. It supports the Cocoa Horizons Foundation which aims to shape a sustainable future for cocoa and chocolate.